Private builders often find themselves unprepared to face the tax consequences upon completion of their work. It is extremly important to obtain a professional advice and do careful tax planning ahead of any project.

Amongst other things to be aware of:

once construction becomes the business carried on for profit, the Primary Residence exemption can not be used and income tax needs to be paid on the net income that was made,

and

in case of newly constructed or substantially renovated unit, HST should be collected on sale price.

In some cases the CRA has to draw a line between a private construction undertaking and a comercial project, and if Primary Residence exemption is disallowed, the tax bill may exceed profits by a substantial margin.

Below are some publications that can help to understand the matter:

Income tax information for builders by CRA

HST information for builders by CRA

HST Guide for builders

General information/tax warnings for private builders

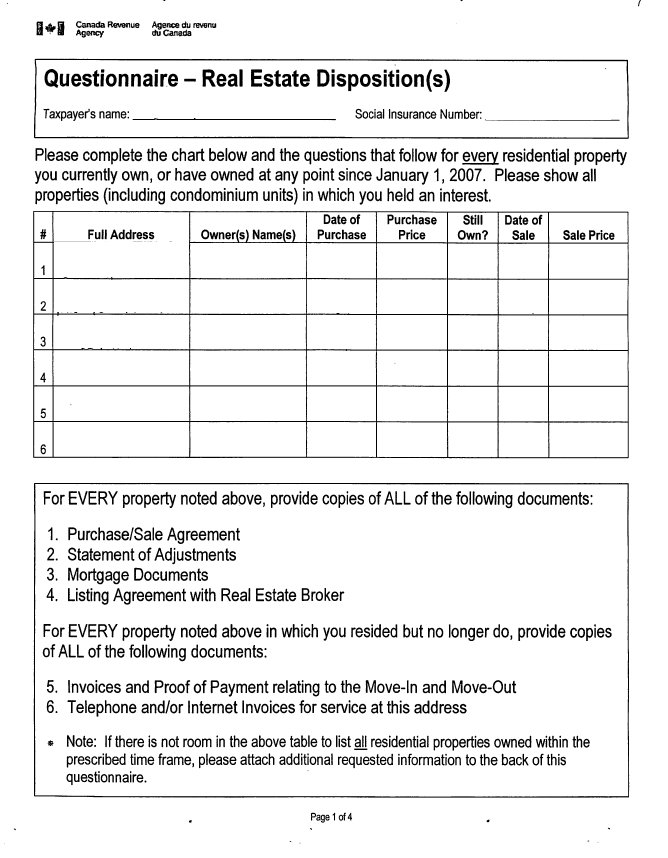

CRA Audit Questionaire - Page 1

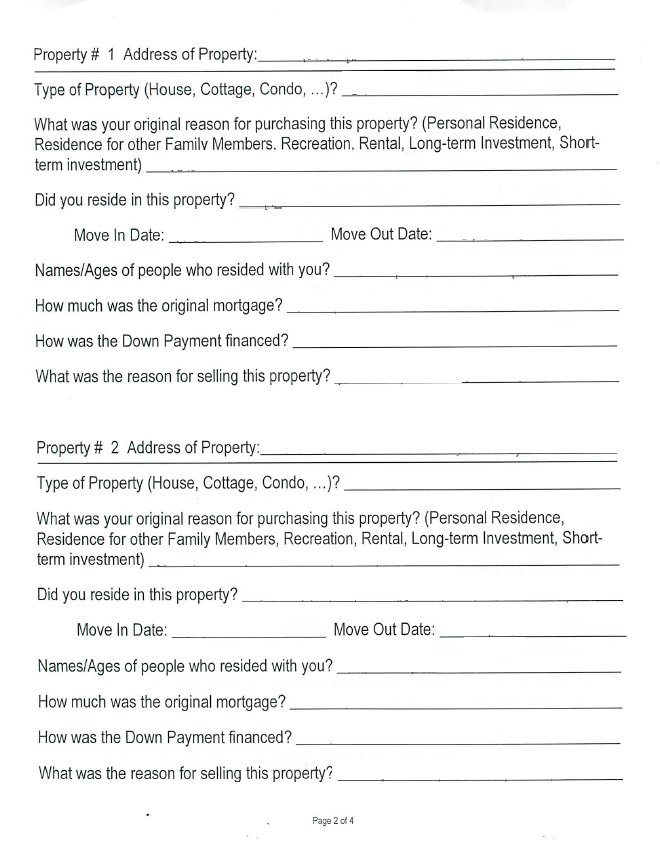

CRA Audit Questionaire - Page 2

CRA Audit Questionaire - Page 3

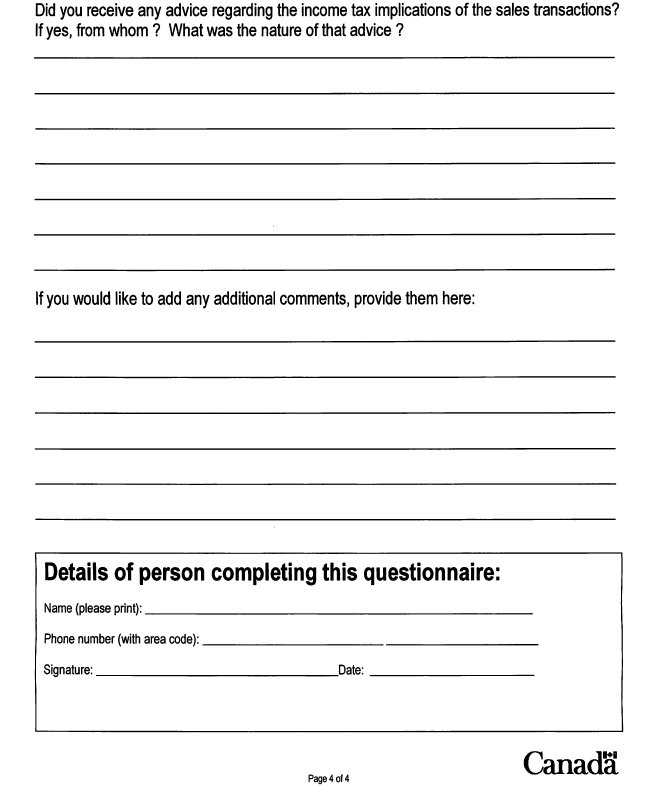

CRA Audit Questionaire - Page 4

Important notice: The information above may reflect a subjective interpretation by the author(s), who, by no means may accept any responsibility or liability whatsoever for the results of proper or improper use of the above information, whole or in part, it as well is explicitly stated that whatever information provided by authors, may not suit specific purpose of specific reader, and it alone may not be relied upon to produce decision. In each individual case professional advice must be obtained.

Back